ESG Is Under Attack – Can It Overcome Its Possibly Fatal Flaw? How ESG Can Fix Its Credibility Issues

It’s easy to pick on a product as obviously broken as ESG. Fresh off another consecutive year of growth, ESG now influences trillions of dollars of investments. But ESG’s flaws and top billing in the US culture wars make it easy fodder for media, CEOs, politicians and investment professionals alike. Like Ben Simmons after “the pass,” ESG is taking hits from all sides. How then should we view ESG in light of this criticism? Will we still be talking about ESG in five years, or are its flaws simply too fundamental to overcome?

The why of ESG

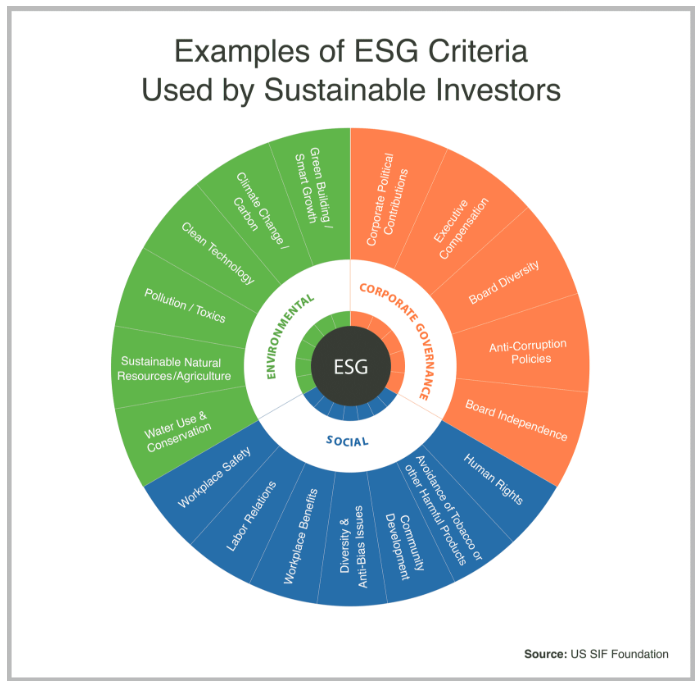

Let’s first quickly review ESG and why we should care about it. ESG, or Environmental, Social and Governance, has become shorthand for socially-responsible investing, or investing with consideration of issues other than pure financial performance. When someone refers to sustainable investing today, particularly in public markets, they are usually referring to the ESG framework and vice versa.

But to call ESG a framework is being generous. It can be more accurately thought of as an umbrella, under which any number of issues to do with a corporate entity’s behavior and impact might fall.

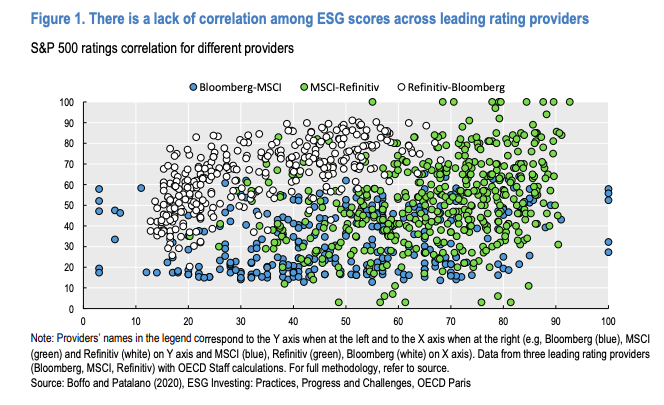

Central to the practice of ESG are ESG scores, which are indicators of an entity’s performance on any given factor or combination of, assigned by ESG ratings agencies and incorporated into investment decisions by sustainability investors and asset managers (See Tesla’s rating from MSCI here). But a common criticism of ESG is that the same entity often receives wildly different ESG scores from different ratings agencies, which calls into question the validity of the whole scoring enterprise.

The size and scope of dollars influenced by ESG (1 in 3 dollars according to US SIF) means that it impacts everyone. ESG is the most widely adopted tool today to align capital with investor values, and it is underpinned by a belief that we have the ability to steer economic activity with an eye towards a longer benefit horizon than legacy market structures that prioritize short-term gains.

How well does it serve its many stakeholders’ needs? Let’s examine how ESG connects each stakeholders’ desires to actions and outcomes.

For investors, including pension funds, retail and institutional investors, ESG directly influences how dollars are allocated to investments. But because of the opacity of ESG scoring and how funds integrate those scores, as well as vagaries in how funds are marketed, it is questionable whether investors are getting what they desire from their investments, and it’s even less clear that the desired outcome, whether reduced financial risk from ESG factors or greater values alignment, is being achieved.

For companies, the need to collect and share ESG data imposes a non-trivial overhead cost, which is especially disadvantageous to some (smaller, less digital) companies. A 2022 KPMG CEO survey finds they are spending over 6% of revenues on sustainability. But on the mildly positive side, the same CEO survey cites some belief that ESG positively impacts the ability to raise capital and attract employees. Still, many CEO’s view ESG efforts as a distracting cost that will be among the first to be cut when expenses need trimming.

For sustainability-focused investment professionals and the companies that serve them, ESG is a boon, generating jobs, fees and technology to manage the integration of ESG with standard investment practices. If ESG is not producing the outcomes investors want, ESG professionals haven’t felt the negative impact to date.

For governments and regulators, ESG is one of the primary tools to understand and influence how their private sectors can make good on national global warming targets. But because of the previously mentioned scoring inconsistencies and lack of penalties for not achieving targets, this use of ESG remains more aspirational than effective.

The verdict is that ESG performs rather poorly in serving its stakeholders. Like a wellness retreat in the 1800’s, ESG helps stakeholders go through the motions, and maybe some good comes from it, but it leaves much to be desired when measured by how well it achieves its goals.

Criticisms of ESG and its potentially fatal flaw

That leads us to the debates about ESG today. At the philosophical heart of this debate is a question that is unanswerable – what are the responsibilities of corporations vs. government for ensuring our well-being, and how do we define well-being universally? While these matters have usually been sorted through the processes of government, the role of corporations in our well-being has never been larger, so it’s no surprise that over 40% of Americans believe the corporate sector should take on more responsibility, whether by choice or regulation. For a good discussion of this topic, I recommend System Error, which lays out the challenges of evaluating the ethics of technology.

Setting aside philosophical debates, we can still find criticisms of ESG from everywhere, including from former practitioners. The New York Times published a substantive article on the difficulties ESG managers faced in defining sustainability in light of the Russian invasion and disruption in global energy supply. FT offered a similar report. Bloomberg and the Wall Street Journal covered how a large share of funds previously classified as “sustainable” are losing that designation, as issuers comply with new guidance on what constitutes sustainable investment. The subtext of all this reporting is that ESG’s position as a proxy for sustainability is on shaky ground. Meanwhile, academic researchers are still looking for a strong correlation between ESG investing and environmental impact or general financial performance, which is perhaps the most telling criticism. We simply don’t know if ESG is effective in what it purports to do, and every misstep: DWS, instances of greenwashing, strains its credibility.

To summarize these grievances, ESG is built upon an inconsistently-defined set of principles about what it aims to measure, is ineffective in achieving its purpose, and has likely garnered investment and resources well beyond its current value.

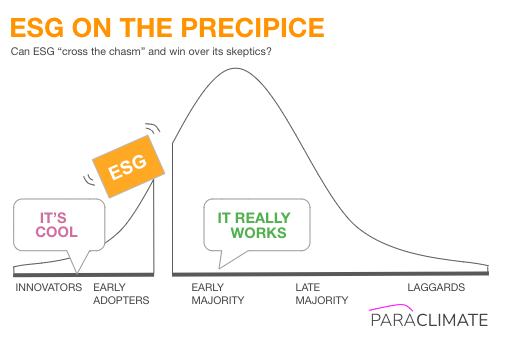

Doesn’t ESG resemble a prototypical V1 tech product? It has found an opportunity in the market and attracted early adopters, but it isn’t adequately satisfying its stakeholders’ needs and is now facing Clayton Christensen’s chasm.

Will ESG be granted enough time to make good on its promises? Many skeptics believe ESG suffers from a fatal flaw of trying to be too many things to too many stakeholders. Today’s ESG attempts to equate financial risk with the intention to do good, but recent events demonstrate clearly those goals are not the same. ESG ratings attempt to make a judgment on the correct balance between environmental stewardship vs. social equity vs. profit-taking, but that’s a multi-variable optimization problem for a complex system that is simply not possible to solve with satisfaction.

ESG may simply attempt to encompass too much under its umbrella to be viable – and any attempt to boil down the virtue of an endeavor to a single score may simply be a bad idea. Paraphrasing Goodhart’s Law, when a measure becomes a target, it ceases to be a good measure. Focusing on the measure causes people to lose sight of the original intent, opening the door for negative consequences.

ESG is simply not a good product, and alternative approaches such as impact accounting aren’t ready. But investors are looking for sustainable investments today, and demographic trends will only increase demand. What should we want in a better investment product?

A sustainable investing wishlist

Whether a v2 of ESG appears to address the shortcomings of today’s ESG, or an entirely different framework arises to meet the demand for better sustainable investment products, I argue that it needs to be aligned with the following principles to be viable long-term.

1. Uses standardized and auditable data as the foundation.

Today, ESG scoring draws from a breadth of disparate data sources that offer no reasonable basis for comparability. Interpretation of that data is mostly subjective and “best efforts” rather than “accurate” or “conclusive.” ESG scores are created through opaque proprietary methodologies that can’t be verified and produce different results depending on who is doing the scoring. These inconsistent scores result from divergences in scope, measurement and weighting according to Berg's Aggregate Confusion research.

The credibility of any future scoring system rests on trust in the data and methodologies underlying the system. The mechanism to establish that trust is to set clear scope and standards for data collection, estimation and interpretation that are transparent, auditable and mutable as needs and capabilities change. With today’s ESG, it’s as if the stakeholders are participating in the same game together but with different rulebooks. Establish and enforce data and scoring standards, likely by industry, region and company size, which will encourage technology and business practices to develop a robust data foundation.

2. Refuses to offer a single metric for “sustainability.”

There is no acceptable way to trade social good for environmental good to arrive at a judgement for which is more virtuous or sustainable. Because there is no reasonable way to assess companies for “sustainability”, any attempt to do so strains the credibility of the whole system. Let’s use more precise ratings to characterize companies’ impacts in this complex world, first by separating the E, S and G components, and then by considering whether those should be separated further.

3. Prioritizes comprehension over comprehensive.

Comprehension and complexity are at perpetual odds. When the purpose is to establish trust, as we aim to do in this future framework, we should lean towards comprehension and explainability over complexity or completeness. A measure that’s not easily understood is doomed to misinterpretation, with ill effects. Practically, that means applying more rigorous prioritization on what aspects of a company’s behavior we aim to measure, and requiring modeled data obtained via AI or other techniques include explainability for how that data was derived and its sensitivities.

4. Clearly separates the scoring for financial risk from the assessment of social and environmental impact.

When we wish to analyze a dynamic process, we define the outcomes we wish to measure, then find the metrics which correlate to those outcomes. We have not executed this properly with ESG metrics to date. Let’s separate the scoring for a company’s risk entirely from the scoring of its environmental and social performance. Then we can tackle how to measure for those outcomes separately and remove another source of confusion and credibility erosion that plagues today’s ESG.

While these principles may seem simple enough, reality will demand compromises for the foreseeable future. The desired data will be unobtainable for a variety of reasons – from privacy rights for social data to general impracticality of collecting it. While social data may always be challenging to obtain, investment in carbon and supply chain analytics, digital transformation, as well as better AI and modeling tools make quality environmental data increasingly viable. While continued dollar inflows into the ESG ecosystem means ESG incumbents don’t have an incentive to make radical changes, rising dissatisfaction with today’s ESG and increasing public support for stakeholder capitalism may create the opportunity to put these principles into practice sooner rather than later.

ESG organizations and companies to watch

While organizations like Ceres and the ISSB are working to improve the current state of ESG, we should all hope they recognize that the future of sustainable investing requires more than an evolution of the current framework. Who are some of the most interesting organizations working in sustainable investing?

ESG Convergence: Industry effort to bring ESG metrics to private markets.

Carbon Collective: One of many robo investors that help direct retail investor funds thematically.

MIT Sloan’s Aggregate Confusion Project: Academic effort to improve ESG measurement.

CRUX: ESG data pipelines and integration service makes data more widely available.

Climatiq: Climate impact data service that is improving how GHG emissions are calculated.

Carbon analytics platforms: See my previous article.

LTSE: Led by Eric Ries, a securities exchange built “for companies and investors who share a long-term vision.”

ESG_VC: Initiative led by VCs in the UK to bring ESG reporting to early stage ventures.

Though ESG may sometimes look the part of a v1 tech product, it remains one of the largest tools we possess today to direct global capital towards a better shared future. Let’s hope we get it right quickly.

Interested in hearing more? Subscribe and follow @greenwashalert. Comments or suggestions? Please reach out. I'd love to hear from you!

MORE ESG READING

Overview of ESG ratings from Bryan Tayan, Corporate Governance Research Initiative at Stanford GSB: link.

Former Timberland COO Kenneth Pucker on the failures of ESG and corporate sustainability: link.

ESG challenges by OECD, 2020: link.

On short-termism: link.

NYU Stern metastudy on ESG performance: link.

GOP vs. Woke Wall Street, New York Magazine: link.